Around June every year, something wonderful happens. Our politicians gather and spend days arguing – huffy and red-faced – about how to spend money.

You may roll your eyes at the thought of white, middle-aged men debating spreadsheets and numbers, but don’t underestimate the significance of budgeting.

Budgeting is essentially tracking income and expenses to understand where all your money is going. Budgeting is a plan or your money.

There’s no perfect, one-size-fits-all budget.

There are several ways to budget. Large companies pay people thousands to fill elaborate spreadsheets and quarterly cash flow budgets. There’s zero-balanced budgeting, static budgeting, annual budgeting – the list goes on.

Everyone will tell you how to budget. “Spend less on x, more on y. Give up coffees. Spend 2.3% of your income on hand-lotion.” But here’s the truth:

There’s no perfect, one-size-fits-all budget. A budget should consider your specific financial needs and goals, and be tailored personally to you.

So, with that in mind, I’m not going to tell you how to spend your money each week. Instead, we’ll look at why and how to start budgeting, and my reflections on what does and doesn’t work. Looking for something else? There are plenty more posts about budgeting here.

Why does budgeting even matter?

We all have that one disorganized friend who doesn’t plan in advance. They’re constantly late, and probably messy.

You want to buy shiny new things, go on a holiday (or seven), and maybe even buy a house one day, right?

Well, you’ll need a plan to achieve all these goals. Otherwise you’ll be a financial mess without a plan, much like said friend.

Have you ever tried baking without measuring the ingredients? It’s a disaster.

If financial wealth is a cake, spending and saving are ingredients. Unless you measure your ingredients with a budget, you’ll end up with sourdough.

How do I even start budgeting?!

- Write down your expenses

- Identity trends

- Set some financial goals

- Find what works for your

Write your expenses down for a week (or a pay cycle). You could use a notepad, a spreadsheet, bank statements. If you’re ultra lazy, use an application that does all the work for you. I’d recommend Pocketbook.

Simply knowing where your money is going puts you ahead of most people. 86% of Aussies don’t know their monthly expenses, according to a 2018 UBank report.

Tracking your expenses can be empowering and confronting. But it’s important to be honest with yourself during this first phase. Even if you’ve overindulged, you need to confront your spending habits.

Once you’ve done this for a week, do it for three more. Now you’ll have a month of expenses to comb over. This can be eye-opening!

Look for trends in your spending habits. Where is all your money going? Are there any reoccurring monthly expenses like insurance or subscriptions?

Write any reoccuring fixed expenses down, and the date these need to be paid. Fixed expenses are the things you need to pay and tend not to change, like rent or a morgage. Variable expenses, on the other hand, are expenses that change. These might include groceries or outings – things you want.

Now that you’ve got a grasp of where all your hard earned dosh is going, you can begin taking control of your money. You can begin budgeting.

Set some financial goals

Setting goals will give your something to look forward to and help shape your future budget. They might be short-term, like saving for Christmas, or long-term like saving for retirement.

Writing these goals down is important. Not only are you committing to them, but you’re also 42% more likely to achieve them according to one study.

Start by looking at the expenses you tracked above. Look at your total income for a week, and minus every expense. How much do you have let?

If you have less than $0 left, your budget is in deficit. If you have more than $0, you have reached a surplus for the month.

Having $0 by the end of your pay week isn’t necessarily a bad thing, so long as your bills are paid. But it’s not ideal, you should aim to have a surplus.

A deficit, on the other hand, is bad. It means you’ve spent more than you can earned. Maybe you’ve borrowed money or overdrawn your bank account.

Your first financial goal might simply simply be to save some money for the month – to have your budget at a surplus. This is certainly a good place to start, but it’s not great.

Set some SMART goals

SMART goals – Smart, Specific, Measurable, Achievable, Realistic, and Timely goals – are well considered, effective goals. They take a want, and make it achievable by giving a clear plan.

“I want to save money.” Isn’t a SMART goal. There’s no deadline or details. How much do you want to save? To make this goal a SMART goal, we need to flesh it out a bit. A smart goal might look like this:

To save $1000 in a year (or $20 a week).

A simple SMART goal

It specifies an amount ($1000), it’s measurable and timely (end of the year). You’ll need to decide what is achievable and realistic based on your own budget. Here are what some goals might look like:

- To start an emergency fund

- To save for a holiday

- To save for retirement

- To have enough money to start investing

- To buy new equipment

These goals aren’t SMART yet, but you can certainly make tailor them to your personal needs, much like a budget.

Find a budget that works for you

Now you’ve identified a reason to budget (by tracking your expenses), and have motivation to do so (your goals) it’s time to actually start budgeting.

You might choose to use a spreadsheet, an app, a notebook, or just to follow some general rules.

The popular 50/30/20 rule, for example, suggests that you should allocate 50% of your take-home pay to expenses, 30% to leisure, and 20% to building wealth.

While this might work well for some it is a huge generalization. Just as a single parent might struggle to save 20% of their pay, a student living at home is unlikely to spend 50% of their income on fixed expenses.

And that’s why you need to find a budget that works for you.

There are many budgeting methods out there. Spreadsheets and pie charts may seem uninspiring for some, so trial and error when trying to budget is only natural.

At some point you will feel like giving up – numbers aren’t that inspiring sometimes. Re-visit your goals to remember why you wanted to start budgeting in the first place.

My take on budgeting

In case you couldn’t tell, I’m a nerd. I keep spreadhseets for weekly budgets, financial goals, bills, and more. I find budgeting fun. Yes, you read that right.

I use this spreadsheet, and quickly update as soon as I spend something. Knowing you are in control of your money is empowering!

However, I don’t plan my variable expenses in advance. Not even I am that discilplined.

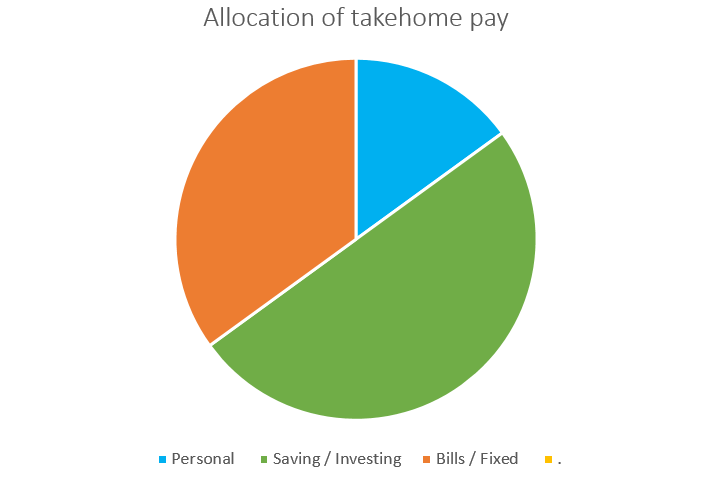

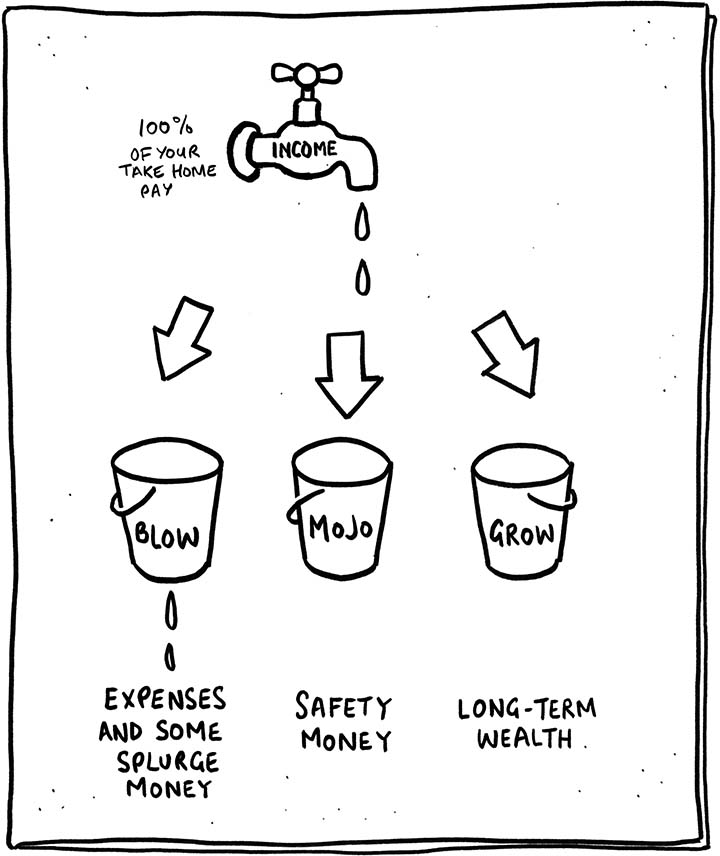

Instead, I spend 15% of my weekly income on whatever I want. I have split my pay so that 15% automatically goes into one account, and this is my fun money. The other 50% goes to saving, and 35% to bills & expenses.

Splitting your pay up into different bank accounts is a very popular, effective technique. It’s The Barefoot Investor’s ‘bucket’ stratergy, which has a cult following for a reason.

What is your take on budgeting? Do you have any tips for our readers? Let me know below!